Soon after Congress passed the $1.9 trillion American Rescue Plan Act of 2021 in March, providing 161 million payments of up to $1,400 per household across the United States, the Biden administration proposed new tax reforms detailed in the $1.8 trillion American Families Plan. The plan aims to address other priorities including education and childcare. The tax code changes detailed in the American Families Plan could have a heavy impact on commercial real estate investors and the industry as a whole.

According to Forbes, individual investors and limited partnerships in the United States control more than $7 trillion in residential and commercial rental property. To pay for programs provided as part of the American Families Plan, the Biden Administration has set their sights on wealthy Americans and high-earning real estate investors. As a result, the tax code changes could fundamentally shift the ways in which real estate is bought, sold and developed.

The Biden Administration has called Congress to make reforms to the following tax codes specifically relating to the commercial real estate industry:

- Eliminate 1031 Exchanges on Real-Estate Profits of More than $500,000

- Eliminate Step-Up Basis on Inherited Property

- Increase Capital Gains Tax

- Tax Carried Interest as Ordinary Income

Eliminating 1031 Exchanges on Real Estate Profits on More Than $500,000

The Biden Administration has proposed to eliminate 1031 like-kind exchanges on real estate transactions with gains of more than $500,000, or to entirely phase out 1031 exchange for real property. 1031 Exchanges (Section 1031 of the U.S. Internal Revenue Code) allow an owner of an investment property to sell and buy a like-kind property within a certain time frame to defer capital gains taxes. The 1031 Exchange code has permitted taxpayers to defer the recognition of taxable gains since 1921.

According to Ernst & Young, approximately 10%-20% of all commercial real estate transactions use 1031 exchange to defer taxes on gains for like-kind properties. It has also been found that the repeal of 1031 exchange would shrink the U.S. economy by $13.1B, resulting in less federal tax revenue. Eliminating 1031 exchange from the current tax code would have a severe impact on future real estate values and overall investor prosperity.

While it is difficult to understand the political arguments on 1031 exchanges, there are many economic benefits 1031 exchanges provide. On March 16, 2021, The Real Estate Roundtable, along with 30 other national real estate, housing, environmental, farming, ranching and financial services-related organizations, wrote to key policymakers to underscore the vital importance of 1031 exchanges. The benefits included U.S. economic recovery, the health of real estate markets, job creation, retirement security, environmental conservation and the preservation of family-owned farms and ranches.

Historically, government parties have made multiple attempts to restrict or repeal 1031 exchanges. These attempts have received a mix of backlash and support depending on the administration party at the given time. The likelihood to reform or eliminate the 1031 exchange code is believed to be possible given the new administration wanting to follow through on their campaign promises.

OF BABY BOOMERS

own one or more investment properties

OF PROPERTIES

acquired through 1031 exchange are sold in a taxable sale

TOTAL JOBS

from 1031 exchange

Eliminate Step-up Basis on Inherited Property

The Biden Administration has proposed to eliminate the step-up in basis on stock, real estate, and other capital assets for gains of $1 million or more ($2 million or more for a married couple). Currently, if a person inherits a capital asset that increased in value when the person who died owned it, the asset’s basis is increased to the property’s fair market value at the date of the previous owner’s death. This adjustment is called a “step-up” in basis. The step-up basis also voids depreciation upon inheritance, reduces complex record keeping and reduces risk of severe estate taxes.

$1 M+ Asset Gain = No Step-Up Basis Tax Exemption

Property donated to charity and family-owned/run businesses and farms would still not be subject to capital gains tax. Also, the existing capital gain exclusion of up to $250,000 ($500,000 for joint filers) upon the transfer of a primary residence would still apply.

While not specifically stated in the proposed American Families Plan, any unrealized gain on capital assets would likely be taxed when the property owner dies. It is important to note – it is not clear how the proposed increase in income tax will align with inheritance tax.

Eliminating the step-up basis on capital assets for gains is difficult to accomplish. Increasing taxes on individuals is more difficult than increasing taxes on businesses. However, it is a good idea to start thinking about how this could impact overall estate planning.

Increase Capital Gains Tax

Elimination of the step up in basis will be amplified if the Biden Administration proposal to increase capital gains tax passes as well. Currently single filers taxpayers earning over $446K are taxed 20% on capital gains and joint filers taxpayers over $502K are tax 20%. Under the new proposal, taxpayers earning $1 million or more annually, long-term capital gains would increase from 20% to 39.6% (Note: 39.6% plus 3.8% surplus net investment income tax = 43.4%). Wealthy Americans would also be impacted by short-term gains. Short-term gains are currently taxed

at the ordinary income tax rate (37%) however, the new proposal increases the top tax rate on ordinary income to 39.6%.

Once a property investment is past the point of diminishing return due to tax increases, the interest in the purchase of property will be dissolved. Congress will have an upward battle to this reform. Again, increasing taxes on individuals is more difficult than increasing taxes on businesses.

"Rewarding risk by a capital gains rate that is lower than the ordinary tax rate, allowing real property to be traded with some tax deferral, recognizing that risk is not just the risk associated with cash investments and allowing a carried interest in a real estate transaction to quality for capital gains, together encourages the productive risk-taking that spurs investment in economically struggling communities and more challenging assets, like affordable housing, and in more challenging communities."

Jeff DeBoer, CEO of the Real Estate Roundtable

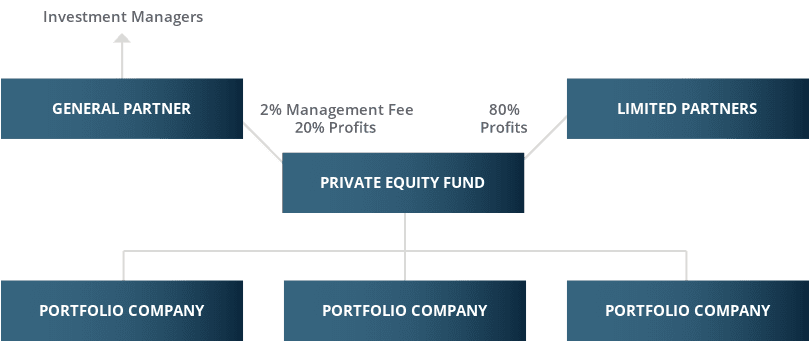

Tax Carried Interest as Ordinary Income

Carried interest is a contractual right that entitles the general partner of an investment fund to share in the fund’s profit. These funds invest in a wide range of assets, including real estate and development funds. Under the current tax code, carried interest is considered a return on investment and is taxed at the 20% capital gains rate. Under the new proposal, carried interest tax would be taxed at the regular income tax rate, which has been proposed to increase to 39.6% for taxpayers earning more than $1 million. See below for a brief recent history of tax reform against carried interest.

A Typical Private Equity Fund

Looking Forward

While the above proposed tax reforms stated in The American Families Plan are in the early stages of legislature, there are still many details that need to be clarified. While none of these tax proposals have hit the Congress floor – except for the carried interest reform – it is important to keep a close eye on how these tax proposals may unfold. We do expected changes will happen, but only time will tell what the result of these changes will be.

It is important to note these reforms have not taken effect as of today; exploring the possibilities of net lease real estate dispositions, acquisitions, and/or 1031 exchanges before these changes gain more ground and potentially pass is always possible. If you are interested in getting more information, feel free to contact SRS NNLG or reach out directly to any of our licensed Real Estate Professionals.