What do our retail real estate experts see for the industry for the remainder of 2018?

SRS’ annual company Summit brought our brokerage teams from across North America to San Diego in February for two full days of knowledge sharing, networking, fundraising, and celebrating another great year. The state of the retail industry was ever present in conversations, presentations, and round table discussions, with seven dominant themes for 2018 emerging through those observations. Below you’ll find our experts’ thoughts as we explore portfolio optimization, continuing store closures, creativity in filling vacant space, the tenant mix evolution, the growing importance of experiential retail, stores of the future, and the strongest-performing investment assets.

1. Portfolio Optimization has Never Been More Essential

For existing retailers, portfolio optimization is the game you need to play to win. Today, every store needs to be a great store, and when you have a large existing portfolio, that is a tall order. Retailers have a responsibility to their investors to grow the bottom line. Those with a small number of locations do that by opening new locations to pull in new customers. Larger, more established retailers continue to grow in that manner, but they must also look to their existing stores to grow revenue by evaluating store performance and occupancy cost. “Many retailers put off managing their portfolios because the task can seem daunting. They need to be in the right boxes in the right locations at the right size with the right occupancy cost,” said Steve Dawkins, COO of SRS Real Estate Partners. “In today’s climate, optimization is no longer an option, it is absolutely crucial for the brand’s survival.”

Strategic retailers are doubling down on successful stores and closing underperforming stores. As we’ve seen in the lists of store closures, the stores that are closing are not typically first string locations. And sometimes it requires closing two stores to open one in a better location. Retailers are also reworking store footprints and adjusting digital strategies to drive local traffic and create better customer experiences. Whatever the strategy is, the focus should be on getting maximum value out of your occupancy cost. In a future blog post, we will further explore the strategies SRS employs to help retailers optimize their portfolios.

WHAT RETAILERS SHOULD KNOW: If you aren’t executing a portfolio optimization plan, the time to start is now.

2. Store Closures will Continue, but on a Much Smaller Scale

To recap, retail closures hit a record high in 2017, with most sources reporting around 7,000 stores having closed. While stores will continue to close in 2018, the scale is not nearly as massive, with predictions landing at about half of what we saw in 2017.

Retailers shutting stores are facing a host of challenges, with the biggest being intense competition from brands that have adjusted well to consumers’ preferences and spending habits. Those that are floundering are struggling to stay relevant in a quickly changing retail environment.

E-commerce is an easy scapegoat as an annihilistic threat for traditional retail. However, even retailers that started online know that brick-and-mortar locations are a crucial part of their brand strategy. As such, the U.S. Census Bureau reported that e-commerce still only accounts for 8.5% of total retail and food service sales.

Store closures are nothing new and have always been a part of the strategy, as we’ve explored in a previous post. To drive that point home, all predictions for 2018 show more stores opening than closing, with estimates near 3,600 new stores for the year in categories such as grocery, health and beauty, service and convenience, and discount retailers. “If brick-and-mortar retail was going to die, it would have happened already. Online sales have been around for more than 20 years,” said John Redfield, vice president of SRS’ Investment Properties Group in the Newport Beach office. “Retailers have to change and adapt, they can’t be stagnant or they will be out- positioned in today’s market. Store models have changed and the space left by outdated concepts has created opportunity for those retailers who have adapted to accommodate the current and future consumer.”

WHAT RETAIL REAL ESTATE PROFESSIONALS SHOULD KNOW: Brick-and-mortar isn’t dying, it’s adapting. Store closures are an inevitable piece of that evolution.

3. Creativity will Play a Big Role in Filling Vacant Space

As stores close, who is taking all of this vacant space? Department store spaces, which are typically some of the most challenging due to their size, have attracted restaurant and entertainment uses, fitness centers, and some are being used for fulfillment of online purchases as landlords are motivated to backfill space with uses that will continue to drive traffic. Big boxes face a similar challenge as there are only so many uses that can take such large spaces. That has led to some creative uses, including medical users, call centers, offices and churches. Vacant small shop space, like those left behind from struggling apparel retailers, are also attracting new and interesting uses. Pop-up shops in these smaller spaces often bring unique product lines or seasonal offerings with some of them drawing a crowd from their big online followings, which can bring new shoppers to the center.

WHAT RETAILERS SHOULD KNOW: Landlords are increasingly open to creative uses to fill vacancies.

4. Craft Retail and Entertainment will Lead the Tenant Mix Revolution

The balance of a tenant mix can be delicate, and the consumer preferences shifts within the industry have completely upset what had been an ideal strategy for years. Some trends are emerging that mark major shifts towards tenants having more control. Shorter lease terms are starting to be the rule rather than the exception as retailers are demanding more flexibility. Retailers are no longer comfortable trying to look 10 or more years into the future. This flexibility is making it more feasible for local concepts to open stores rather than just regional and national brands.

Craft retail, a term we have embraced here at SRS to describe the retailers emerging on the scene that specialize in a more customized product or experience, has become the darling for shopping center enhancement. In stark contrast to stores with mass produced items that are easily found at any location or online, craft retailers represent a more curated, personalized and locally-relevant experience, and consumers relish “discovering” something new, a great deal, and taking home something unique. The same goes for restaurants. It is often now the chef-driven restaurants that provide a unique local experience and are increasingly becoming key traffic generators for shopping centers. Much like the craft beer revolution, that has seen market share shift away from the mass produced conglomerate brands, craft retail provides consumers a unique experience that they can’t get online and builds a connection to their local community, which has them coming back again and again. We’ll dive further into the increasing presence of craft retailers and restaurants in shopping centers, the impact they can have, and the lessons learned by our experts in a future post.

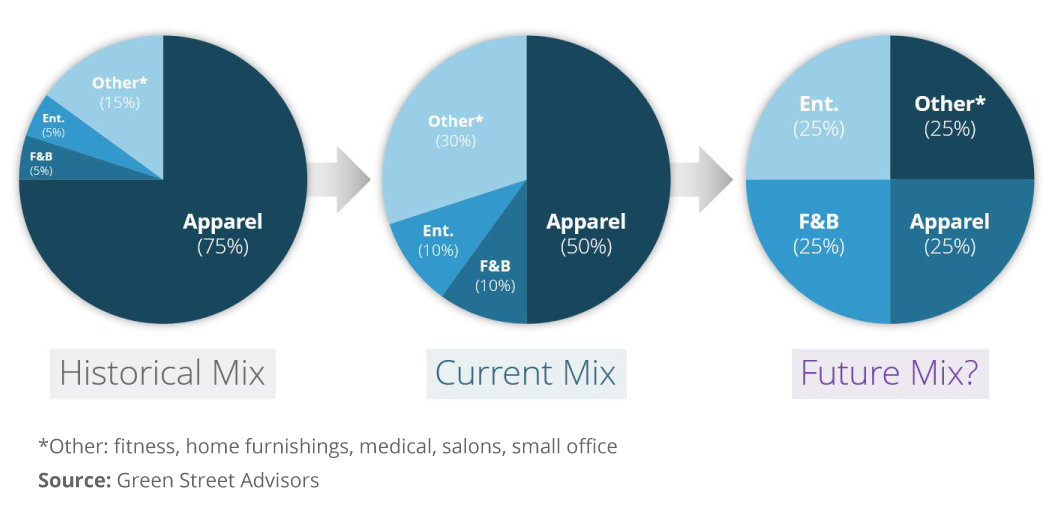

So, how are these changes affecting the ideal tenant mix? Historically, apparel has accounted for approximately 75% of the space in a retail center, with food and beverage and entertainment each taking 5% respectively, and the remaining “other” category accounting for 15%. Currently, the more ideal mix takes apparel down to 50%, bumps up food and beverage and entertainment to 10% each, and other doubles to 30%. All signals are pointing toward the future mix being more evenly spread, making the experiential tenants such as restaurants and entertainment concepts and craft retailers accounting for 50% or more of the presence within a center. What exactly is in that “other” category you ask? Well, it’s fitness, medical, salons, small office, and home furnishings that are filling the balance of today’s vacant space.

WHAT RETAILERS SHOULD KNOW: Retailer, restaurant, and entertainment users focused on the local consumer experience are the new darlings for shopping center enhancement.

5. Millennials will Continue to Drive the Experiential Retail Revolution

Millennials’ influence on society is ever-growing and in 2017 their preferences certainly changed the retail landscape in some unexpected ways. But, retailers are recognizing that millennials represent the future for their stores. Retail brands are learning how millennials prioritize spending on experiences and events over products, and are attracted to places that are fun to share on social media.

Enter the food hall — multi-faceted markets showcasing a variety of local food vendors and artisans, and a haven for all things that appeal to millennials. Food halls aren’t new; in fact, many major cities have had at least one food hall for years, and Europe claims to have a food hall style market that is over 800 years old. However, this ancient concept is finally getting its starring moment in America, with the current count of approximately 100 U.S. food halls expected to double by 2019.

“Properly curated food halls are more than just a dining experience. They create a feeling of community. People feel they are connecting to the environment around them. Restaurants are local, and for them it is a passion, and the product they are serving comes directly from that passion. Visitors feel good about supporting the local businesses, as well as putting their dollars into the local economy,” said Kirk Williams, managing director of asset management for Cypress Equities. “But food hall curation and operation can be difficult. You have to have a sense for it and be ready for the battle. Every tenant requires special attention, making sure they are successful, as well as keeping an eye out for emerging talent to bring in when and if a stall opens up. Food halls aren’t tied necessarily to a specific type of center, however, a consistent theme is that there needs to be a strong signal that the property is invested in the community. And don’t forget, a lot of attention and management is needed in order to be successful.”

Entertainment is exploding as a result of the experiential preferences of consumers, and theaters, bowling concepts, escape rooms, lounges, and similar gathering spots are nearing requirement status for a successful larger retail center, or lifestyle retail center. Traditional fashion and apparel is continuing to trend towards fast fashion or off-price retailers, while unique and customizable fashion and lifestyle brands, such as Bonobos, Rent the Runway, Fabletics, and Warby Parker are all growing their presence. Fitness clubs and boutiques, as well as co-working spaces are blending retail with amenities, making centers a convenient spot to hit all of your needs.

WHAT RETAILERS AND LANDLORDS SHOULD KNOW: Elevating the experience within your stores or your center is vital to long-term success, especially with millennials.

6. The Stores of the Future are Beginning to Arrive

SRS’ CEO, Chris Maguire, thinks shopping center owners need to be prepared for the proliferation of unstaffed stores like Amazon’s cashierless convenience store concept, Amazon Go.

“Glimpses of that sort of model have been around for a while, with kiosk ordering available at many McDonald’s and Panera Bread locations, or the cupcake ATM at Sprinkles Cupcakes. Amazon’s move into the space isn’t the first, but it will amplify the attention on using frictionless technology to drive new innovations for the consumer experience that will likely be adopted by more and more retailers.” said Maguire.

Amazon has discussed in recent interviews licensing the in-store technology to other retailers, but competitors aren’t waiting on Amazon’s entry into the market, with several rolling out their own automated systems. Walmart’s Scan & Go system, a downloadable app, allows customers to scan and bag items, including produce, while they shop and pay directly with their phones. Walmart is already testing the technology at 100 stores across the nation. Kroger implemented a similar system called Scan, Bag, Go, which allows customers to use a wireless handheld scanner or the downloadable app on their personal device to scan and bag products as they shop for a quicker, seamless checkout experience. Their program is being piloted in 18 stores, and both Walmart and Kroger developed their own technology, showing just how important they believe this type of innovation is to the stores of the future.

Even restaurants, which have been mostly considered Amazon-proof, are shifting how they interact with customers. Food delivery has become increasingly convenient, allowing consumers to dine at home on just about any kind of food they like. Even fast food chains are getting in on the delivery game. Many are partnering with services such as Uber Eats, Door Dash, Grub Hub, and yes, Amazon Restaurants, who provide the drivers and the ordering technology.

On the horizon, technology development is making it more and more feasible for the store of the future to compete with online delivery behemoths like Amazon and Walmart. Robomart is currently piloting a driverless, autonomous grocery store on wheels. It drives fresh produce straight from the supermarket to the customer, and grocery chains can license the platform and the vehicles, which allows for another consumer channel while leveraging the in-place supply chain.

WHAT RETAILERS SHOULD KNOW: Using technology to enhance the in-store consumer experience can be a differentiator today, but tomorrow it will be a necessity.

7. Core-Area and NNN will Headline Investment Deals

As SRS experts discussed at the end of 2017, investors remain attracted to well-conceived and well-positioned multi-tenant assets, but REITs are continuing to shed non-core assets as they shift focus to their top performing properties.

Pierce Mayson, principal of SRS’ Investment Properties Group in the Atlanta office, said “Last year was marked by a period of price discovery for buyers and sellers as the market experienced a notable disconnect on the value of multi-tenant retail assets, providing sellers with an easy choice to refinance rather than sell at what they perceived to be a discounted exit price. However, rising interest rates and acceptance of a changing retail climate have narrowed the gap, making the decision to refinance a much more difficult one; while creating improved conditions for a meeting of the minds between buyers and sellers in 2018.“

One sector that has stayed consistent throughout the changes within retail is the single-tenant net lease sector. National Real Estate Investor’s recently released Net Lease Research report stated that with the opportunity for long-term leases to stable tenants, the sector remains popular with a variety of commercial real estate investors. NREI is confident that the sector will remain in solid shape for the foreseeable future.

Managing principal of SRS’ National Net Lease Group, Matthew Mousavi agrees, saying, “Net lease will continue to be an attractive investment and asset type for a wide range of investors. Investors will always have demand for passive yield backed by a tangible asset. Increasing interest rates and other shifts in the market should result in more attractive opportunities throughout 2018 from the investors’ perspective. Increased merger activity, changes in healthcare, the ‘Amazon’ headlines, and next-generation retail will continue to alter the look and feel of the sector. Food uses, lifestyle, entertainment, health and wellness, as well as value-oriented retailers, should continue to outperform other categories and drive continued investor demand.”

WHAT INVESTORS SHOULD KNOW: Single-tenant net lease investments will continue to perform well and well-located multi-tenant assets will continue to keep investors interested.

Our collective knowledge and exclusive focus on retail help better position you for success in the changing retail landscape.

It’s always an eye-opening experience when you bring together so many top-level retail real estate professionals to openly share their knowledge. One thing is clear, we are as excited as ever about the retail business and thrilled to help shape its current transformation. If you need help with real estate strategy in this brave new retail world, please reach out to Janie French, SRS’ vice president of business development.

We always enjoy having our team members together to celebrate and collaborate. To see some of the fun we had at our Summit, view our Summit 2018 video. If you have interest in joining a retail real estate platform that has this much fun and genuinely collaborates, reach out to Woody McMinn, SRS’ president of North American brokerage.