Market Trends Review & Forecast

As Covid-19 restrictions ease and the economy continues to open, retail sales have jumped. The National Retail Federation expected retail sales to jump between 10.5% and 13.5% to more than $4.44 trillion in U.S retail spending in 2021 compared to 2020. This forecast is nearly double their original growth forecast given in February 2021, which was between 6.5% and 8.2%. Much of the increased growth in retail spending is attributed to continued vaccine distribution, shoppers spending government stimulus checks and private sector ingenuity.

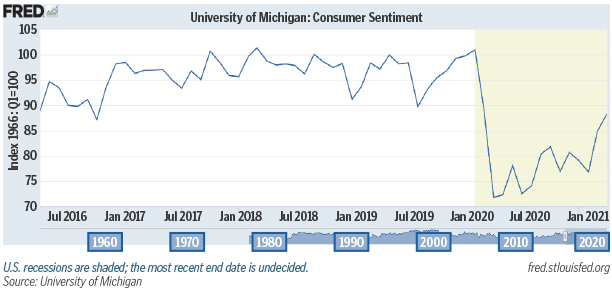

Despite the overall retail sales growth projections, consumer sentiment dropped in May 2021 to 82.9. While this is an increase from one year ago, consumer sentiment dropped 5 points from April 2021. May’s dip is largely attributed to the raising prospects of inflation. The University of Michigan reports inflation concerns are the most prevalent they have been over the last 50 years as inflation is expected to last longer than many government officials anticipate.

U.S. Retail and Food Service increased by 24.4% YOY as of May 2021, which proves the resilience of the overall retail industry. This sharp rebound breaks down to retail trade sales recording an increase of 26.9% YOY, while clothing and clothing accessories stores were up 200.3%. Spending should continue to show strength during the second half of the year as high savings and growing employment income take over from the initial burst of spending fueled by stimulus checks. As we focus on the second half of 2021 and beyond, below are key indicators to note as the retail industry continues to rebound.

2021 Key Indicators

QSR Digital Transformation

- Frequent Demand Menu Changes

- Detailed Expense Tracking

- Drive-Thru Services Accommodation

- Digital Kitchens

Grocery Stores

- Digital Orders/Contactless Payment

- Ecommerce Grocery

- Landscape Transformation

- New Contactless Services/Smoothie Making

- Machines & Salad Robots

Evolving Customer Behavior

- Live Streaming Shopping/Social Commerce

- Ecommerce Sites & Contactless Payment

New Amazon Platforms

- Amazon 4 Star

- Amazon Fresh

- Amazon Pop-Up

- Amazon Go/Go Grocery

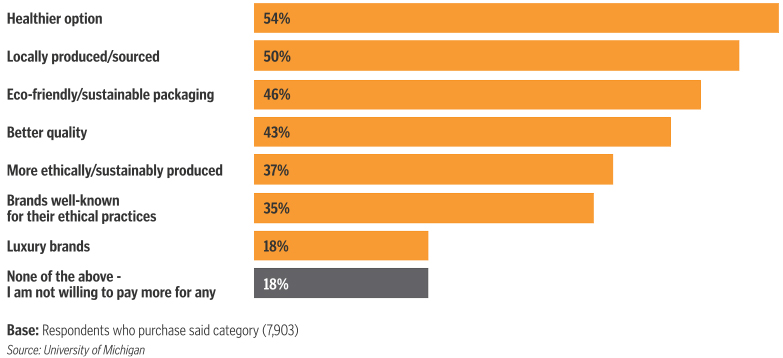

EXHIBIT 5: FOOD FEATURES COMSUMERS ARE WILLING TO PAY MORE FOR

Q: For the following product catefories, which attributes would you be willing to pay more for? (Grocery including general food and beverages.)

2021 Economic Review & Forecast

COVID-19 Vaccination | 315 million (52%) people in the U.S. have received their first dose (June, 2021)

Startups are Growing | 500,200 New Business Applications in May 2021 (up 69.7% YOY)

Evolving Work Force Environment | Remote Work & Space Hybrid Conversions

Liquid Deposits | Increased by 3.2% since December 2020

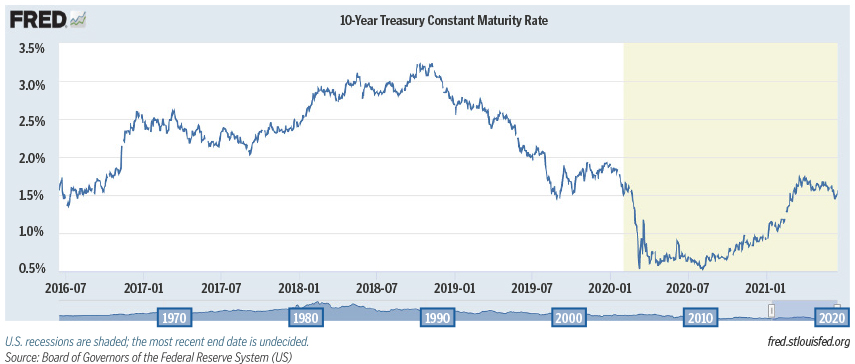

10-Year Treasury Note | Expected to rise to 2.2% in 2021, up from the current rate of 1.57%* This increase could create challenges for buyers to obtain ideal financing.

Inflation | Expected to rise 3.4% in 2021, up from 1.7% in 2020*

GDP | Expected to grow 6.6% in 2021, up from -5.8% growth in 2020*

*Source: Kiplinger Forecast & Reuters

Although the yield on the 10-year Treasury fell as Fed announced they expect to increase interest rate by the end of 2023, yields are expected to increase due to the growing pressure of inflation. Democrats are in a position to pass a $2 trillion infrastructure spending bill, which would be expected to boost economic growth and continue to push up both inflation and interest rates. The 10-year Treasury rate is expected to rise to at least 2.2% by the end of this year.

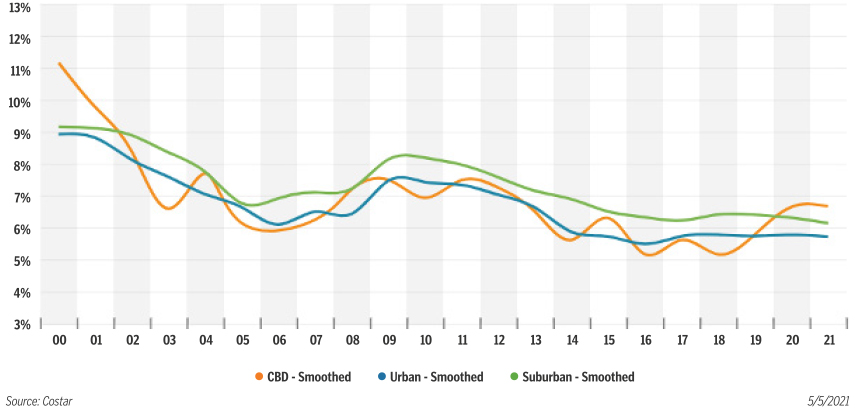

National NNN Retail Cap Rates by Location Type

Average Summary Report – Cap Rates by Industry Sector

For this report, SRS reviewed Q2 2021 sales reported by Costar for the following sectors: Automotive, Bank, Big Box/Superstore, Casual Dining, C-Store/Gas, Dollar Stores, Educational (Childcare), Fast Casual, Grocery, General Retail, Medical STNL, Pharmacy, and QSR. In Q2 it’s especially important to understand the impact the ongoing pandemic has had on the relationship between length of lease term and capitalization rates across all product types, as well as how the pandemic has affected buyer bias toward certain sectors. To do so, we compiled the following average summary reports for a number of data points throughout each mentioned sector. As can be expected, sectors classified as “essential business” with more capabilities to adapt to a changing marketplace have been less affected than others. Note: this report captures data only for transactions which have reported a sale price and capitalization rate. The following data has been collected from sources deemed reliable; it may not include confidential and/or proprietary information of the marketplace.

AUTOMOTIVE

Sales of new vehicles in the US remain healthy but are showing signs of a slowdown due a lack of new car inventory caused by a shortage of semiconductor chips. The chip shortage caused automakers to cut vehicle production, leading to a demand shift toward quality used cars in 2021. The shift toward used car supply has helped with overall sales as 4.5 million vehicles sold in Q2, a 52% increase compared to one year ago. The inflated cap rate of 6.03% can be attributed to higher price points within the sector, with the average $/sf increasing by more than 50% over the previous quarter.

BANK

As the bank industry recovers for the impact of Covid-19 and digital banking concepts grow, bank branches continue to pivot to new business models. Bank institutions that made strategic technology investments prior to COVID-19 have come out stronger. Banks continue to be a focus for investors given the strong credit of the tenants. The average cap rate for bank properties sold in Q2 inflated by 45 bps over the previous quarter – largely because average lease terms in the sector decreased by 4 years. The sector has held relatively steady in the high 5 to low 6% cap rate over the last 12 months.

BIG BOX/SUPERSTORE

The big box sector within net lease continues to see diminished activity due to the pressure of online consumer spending and evolving square footage and business restructure. Since the pandemic, we have not seen a quarter with more than 10 trades in this asset type. Diminished activity is expected to continue through the second half of 2021 as owners are tasked with trying to resolve big box space use options. Cap rates for Q2 recorded at 6.23%, while the average lease term dropped to 6 years from 8 years in Q1.

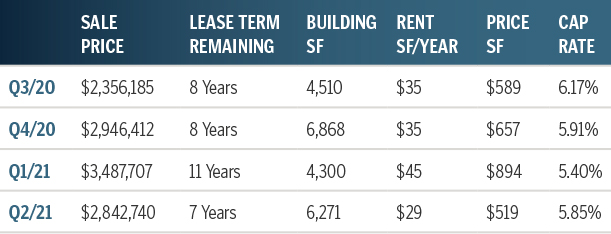

CASUAL DINING

The impact of COVID-19 has forever changed most casual dining restaurant business functions and as a result had a significant impact on investment sales for this sector during the pandemic. As restrictions have lifted, activity has started to resume to a new business model normalcy. Casual dining companies that were able to adapt to a fast-casual dining models have been able to have the best success. Cap rates compressed by 43bps from 6.67% in Q1 to 6.24% in Q2 as buyers have regained confidence in the product type within stronger geographic markets across the country.

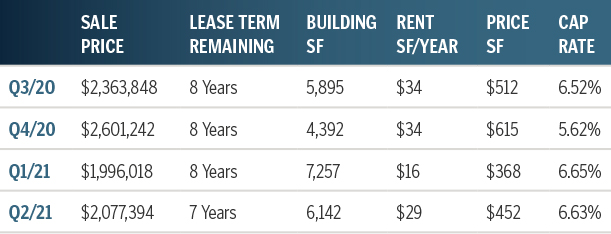

C-STORE / GAS

The c-store/gas station space remains to be a very active sector of net lease given the internet resistant foundation as well as being labeled as an essential business. Revenue for c-stores/gas stations is expected to grow at an annual rate of 2% until 2026. As more people return to work and school, the need for c-stores will increase. Cap rates are increasingly compressing, falling 12 bps from the previous quarter while average lease terms also fell by 1 year – typically these two variables have an inverse correlation. This cap rate compression demonstrates a flight of demand by net lease space buyers.

DOLLAR STORES

The discount dollar sector continues to be one of the most highly sought-after spaces as investors target growth opportunities given high volume of sale transactions being made in comparison to other retail sectors. Expect this sector to continue to outperform other sectors as flight to safety and recession resistance remains to be a target for investors. In Q2, cap rates compressed 37 bps to 6.60% while average term, rent, and price/sf remain relatively flat.

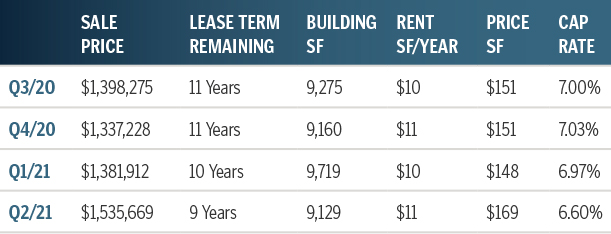

EDUCATIONAL

The demand on the educational sector has been changing and evolving due to the impact of COVID-19. While there has been a growing demand on homeschool companies, more net lease investors are seeking newly developed education space to perform higher yields as on-campus restrictions are lifted. As schools continue to open their campuses to students and parents return to work, cap rates for educational NNN properties compressed by 20 bps in Q2 with average lease terms recording at 9 years.

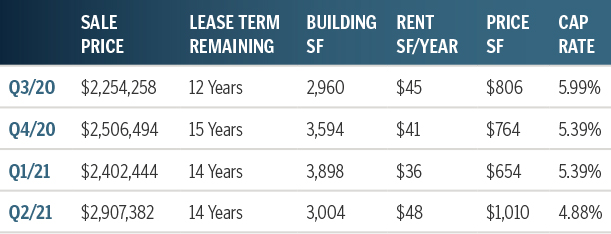

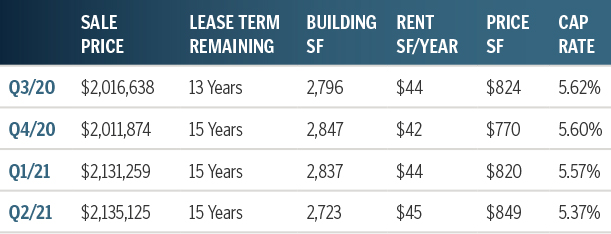

FAST CASUAL

This sector consists largely of credit-worthy brands like Panera Bread and Chipotle. These brands and others in the industry alike have been able to quickly adapt to customer demand by space remodeling, adding drive-thru to permitted spaces and provide in-app and delivery orders. While supply increased (8 in Q1 compared to 15 sales in Q2), cap rates for this sector compressed to 4.88% as major brands like Chipotle and Panera Bread have experienced tremendous growth over the past year and constitue over 70% of transctions in this quarter.

GENERAL RETAIL

General retail sectors include fitness, hardware, furniture, home goods, cellular stores and other retail types which do not fall under one of the other focused sectors. Average cap rates have stayed historically consistent in the mid 6% range, and recorded at 6.63% in Q2. The number of properties trading hands in this sector increased back to historical averages, demonstrating how investors are again looking at the net lease retail sector in general as an attractive, low or zero-management investment market with stable cash flow & sizable returns.

GROCERY

General retail sectors include fitness, hardware, furniture, home goods, cellular stores and other retail types which do not fall under one of the other focused sectors. Average cap rates have stayed historically consistent in the mid 6% range, and recorded at 6.63% in Q2. The number of properties trading hands in this sector increased back to historical averages, demonstrating how investors are again looking at the net lease retail sector in general as an attractive, low or zero-management investment market with stable cash flow & sizable returns.

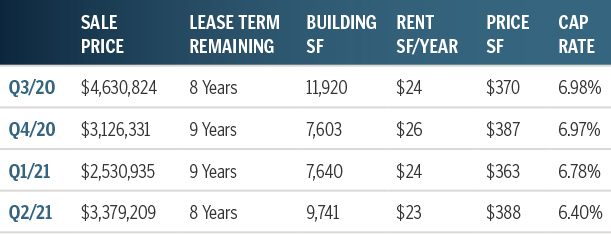

MEDICAL STNL

Given the medical industry has been deemed as one of the most important sectors due to the correlation impact of COVID-19, single tenant net leased medical properties saw a slight compression in average cap rates, recording at 6.40% in Q2. Through the second half of 2021, cap rates are expected to hold steady as most sales transactions in this sector are trading hands in suburban markets. As sales transactions grow into metropolitan markets, we can then expect to see a compression in cap rates.

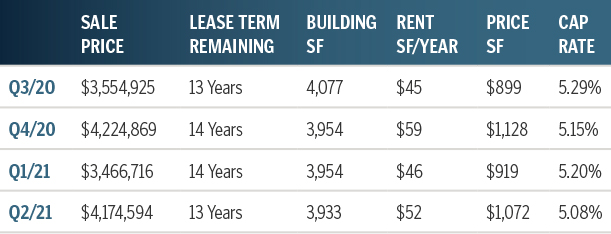

PHARMACY

Average cap rates for pharmacy net leased assets slightly increased by 9 bps in Q2 to 6.15%. As pharmacy stores are being looked at as another shopping alternative for consumers and pharmacists roles have changed given their accessibility to the public as health care professions, it is expected cap rates will remain relatively flat or slightly compressed through the second half of 2021 and into 2022. This sector is largely dominated by Walgreens transactions, and we expect to see the same over the coming months.

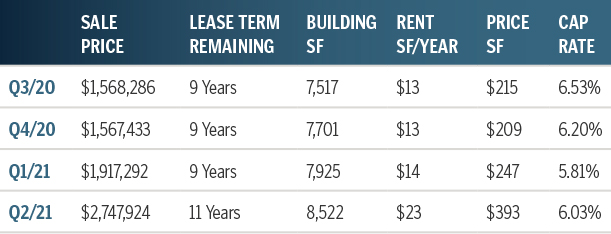

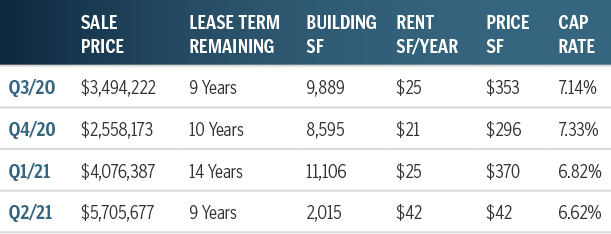

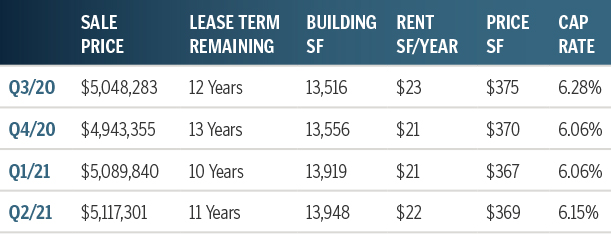

QSR

QSR remains a steady and highly sought after asset type given the sector’s minimal need for adaption compared to other food service providers. Further, QSRs typically offer a lower price point and a higher percentage of absolute NNN lease types for investors compared to other sectors. Cap rates in Q2 compressed 20 bps compared to Q1. It is expected the QSR sector cap rates will remain relatively flat or slightly compressed through the second half of 2021.

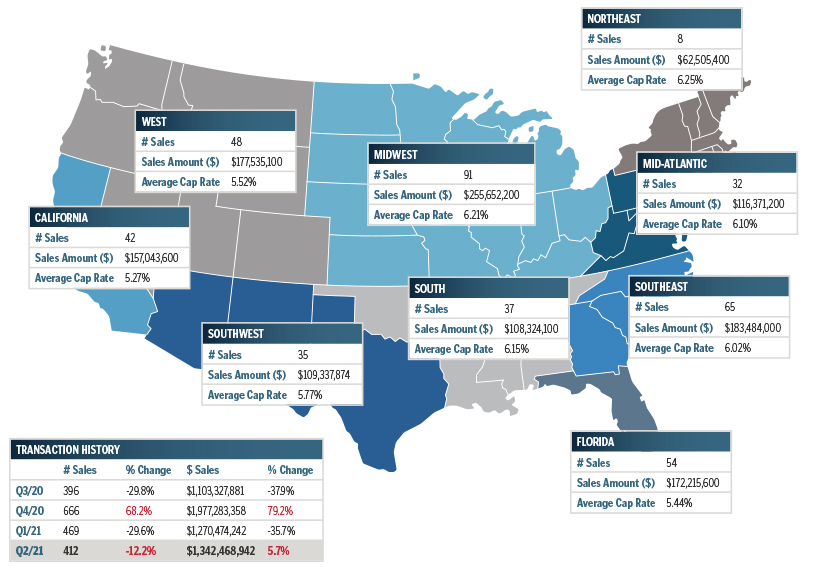

YTD Market Sales Data – By Region

* Market totals represent the study’s sample sizes for select industries and are not indicative of all retail sales that occurred for all of 2020. Analysis has accounted for sales as reported to sources deemed reliable in the following sectors: Automotive, Bank, Casual Dining, C-Store, Dollar Stores, QSR, Medical, Pharmacy, Childcare, Fast Casual, Grocery, Big Box, and General Retail (Fitness, Hardware, Furniture, Cellular Stores, etc.). This may exclude confidential and/or proprietary information.