With the Democratic Party gaining full control of Congress after the January 5th Georgia runoff election, the Biden Administration can now carry out proposed agendas. The Biden Administration and Democratic platform contain numerous proposals for reforming tax codes. The most significant proposal which could impact real estate investment is Section 1031 “like-kind” exchange of the Internal Revenue Code. The Biden administration has proposed to eliminate 1031 like-kind exchanges for investors who make an annual income greater than $400,000 or entirely phase-out 1031 exchanges for real property. The likelihood to reform or eliminate the 1031 exchange tax code is believed to be possible given the new administration wanting to follow through on their campaign promises. 1031 exchanges (Section 1031 of the U.S. Internal Revenue Code) allow an owner of an investment property to sell (downleg) and buy (upleg) a like-kind property within in a certain time frame to defer capital gains taxes. The 1031 exchange code has permitted taxpayers to defer the recognition of taxable gains since 1921.

According to the IPX1031 data, 63% of exchanges feature replacement property (upleg) which is more expensive than relinquished property (downleg).

1031 Exchange Investor Benefits

- Downleg property may have better return, less risk, or offer an opportunity to diversify a portfolio across multiple asset types.

- A property owner can either consolidate values of several assets into one or might want to divide a single asset into several.

- Downleg property may have less property management and/or expense liabilities for ownership.

- Opportunity to invest in growing real estate market locations.

1031 EXCHANGE TAX CODE TIMELINE

Historically, government parties have had multiple attempts to restrict or repeal Section 1031 like-kind exchanges. These attempts have received a mix of backlash and support depending on the administration party at the given time.

1031 Exchange Recent Political Agendas

2014

President Obama proposed a $1 million cap on 1031 like-kind exchanges and then, in 2015, proposed to eliminate exchanges of collectibles, artwork and other personal property. This did not pass.

2016

Candidate Hilary Clinton proposed to eliminate like-kind exchanges for investors making more than $250,000 and to limit its impact on various non-financial assets such as farms, businesses, and real estate. This did not pass.

2017

On December 22, President Trump signed the (HR.1) “Tax Cuts and Jobs Act” tax reform bill. This bill preserved 1031 like-kind exchanges for real estate and exchanges for personal property assets were eliminated. The new tax reform to the 1031 exchange passed and took place January 1, 2018.

The Effects of Eliminating 1031 Exchanges

A September 2020 study led by the Real Estate Research Consortium concludes that eliminating 1031 exchanges altogether would disrupt many local property markets, harm both tenants and owners, and would push offshoring business activity. Also, in 2015, an analysis by Ernst & Young found that either repeal or limitations of like-kind exchanges could lead to a decline in GDP of about $8 billion annually. Such repeal or limitations would largely stagnate business activity and impact jobs for brokers, appraisers, insurers, lenders, contractors, entrepreneurs, developers, REITs, and manufacturers.

Real Estate Roundtable President and CEO Jeffrey DeBoer notes the following ways in which like-kind exchanges contribute to the economic growth and create opportunity for entrepreneurs:

- Exchanges reduce the need for outside financing, leading to less leverage and debt on U.S. real estate. As a result, exchanges allow cash-strapped minority women and veteran-owned businesses to grow their business by deferring tax on reinvested proceeds.

- Like-kind exchanges are important during economic downturns when access to capital is less certain.

- Like-kind exchanges create a more dynamic real estate marketplace, ensuring properties do not languish, permanently underutilized, and under-invested.

The threat to eliminate 1031 exchanges will disrupt real estate investment markets in all 50 states, but especially in high tax states like California, which accounts for 35% of all exchanges nationwide within the past 10 years. According to a study by David C Ling and Milena Petrova, 1031 exchanges in high-tax states varies between 10%-18% of all sales in the respective market.

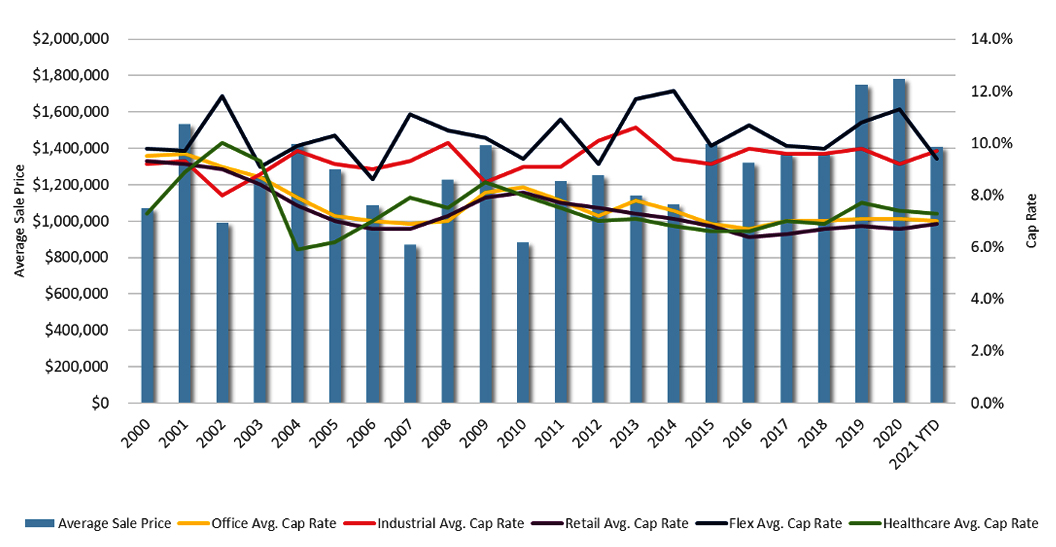

The two tables below showcase 2019 and 2020 NNN/1031 exchanges sales volume covering all sales transactions under $10M for office, industrial, retail, flex, and healthcare product type.

STATE | 2019 NNN/1031 EXCHANGE SALES VOLUME | 2019 NNN/1031 EXCHANGE SALES VOLUME | YTD % CHANGE |

|---|---|---|---|

CA | $512,981,710 | $390,288,144 | -23.9% |

FL | $222,400,696 | $108,886,850 | -51.0% |

TX | $186,103,369 | $164,919,412 | -11.4% |

GA | $124,403,121 | $101,152,868 | -18.7% |

AZ | $103,440,768 | $87,390,478 | -15.5% |

IL | $87,771,755 | $33,086,884 | -62.3% |

NC | $87,187,379 | $60,315,407 | -30.8% |

WA | $82,767,313 | $22,172,738 | -73.2% |

PA | $75,223,112 | $32,761,793 | -56.4% |

MN | $71,346,071 | $62,476,219 | -12.4% |

OH | $63,858,079 | $57,413,018 | -10.1% |

CO | $58,646,223 | $65,494,263 | 11.7% |

VA | $56,289,373 | $23,114,214 | -58.9% |

YEAR | NNN/1031 EXCHANGE SALES VOLUME | NNN SALES VOLUME | TOTAL % OF 1031/NNN |

|---|---|---|---|

2016 | $1,924,037,652 | $7,407,098,809 | 26.0% |

2017 | $2,338,496,832 | $7,614,857,743 | 30.7% |

2018 | $2,210,196,210 | $7,361,279,189 | 30.0% |

2019 | $2,423,201,836 | $9,533,656,489 | 25.4% |

2020 | $1,645,149,417 | $9,220,663,162 | 17.8% |

*Source: Costar. Product Type: Office, Industrial, Retail, Flex & Healthcare

If 1031 exchanges do get restricted, investors would delay disposing of their properties or engage in alternative tax deferred strategies. In effect, this response would reduce the tax revenues collected by both local and state governments. Additional effects would include higher taxes for commercial property owners, decreased property values and increased rental and decreased sales activity.

The main economic benefits of 1031 exchanges are increased investment, reduced leverage and reduced property holding periods. On average, replacement like-kind exchanges are $305,000 (33%) higher compared to acquisitions by the same investor following a sale of a property. Also, capital expenditures (building improvements) in a like-kind exchange tend to be higher by $0.27-$0.40/SF.

1031 EXCHANGE ECONOMIC BENEFITS

- Increase investment volume and additional capital markets in real estate

- Creates positive sale fundamentals for properties that have unrealized capital gains

- Allows a lower income demographic level to invest in real estate

- Shorter real estate holding periods – average to be half a year shorter

- Support jobs and wage growth

- Contribute tax revenues to state and local governments

- Less borrowing debt

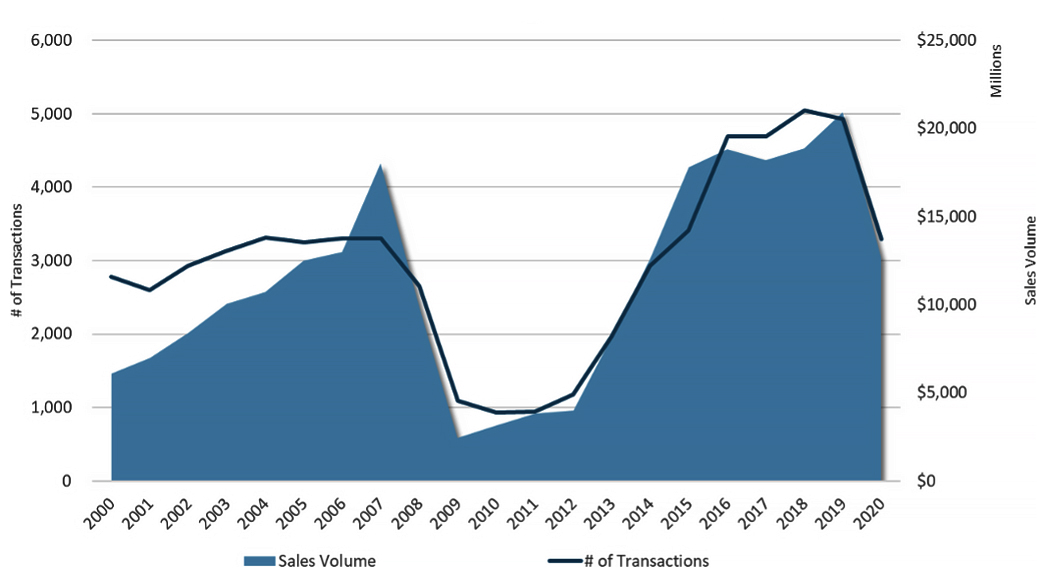

NATIONAL 1031 EXCHANGE SALES TRANSACTIONS

For more insight on 1031 exchanges

Authors

Sources:

1) “The Tax and Economic Impacts of Section 1031 Like-Kind Exchanges in Real Estate” by David C. Ling and Milena Petrova

2) “The Economic Impact of Repealing or Limiting Section 1031 Like-Kind Exchanges in Real Estate” by David C. Ling and Milena Petrova

3) Real Estate Roundtable, “Policy Issues: Like-Kind Exchanges.”

4) Exeter1031.com, “History of Section 1031 of the Internal Revenue Code