The holidays are approaching, consumers are spending, and everyone is looking towards retail to get an inkling of how brick-and-mortar will fare. Many department stores reported strong Black Friday sales, and that’s encouraging seeing that they, more than any other retailer, need a strong end to 2017. The state of the retail industry, with a reported 6,700 store closures this year, has been widely documented and has dominated headlines for months.

Despite the negative attention that has drawn the public’s eye, retail property is considered relatively healthy, with generous capital available to owners and investors according to information collected from retailers, retail real estate executives, developers, REIT executives, lenders, and researchers in PwC’s annual Emerging Trends in Real Estate Survey. Still, even though many sources have reported that there are actually more stores opening than closing this year, unease continues to color the decisions that retailers, landlords, and investors are making in regards to retail real estate.

With the future of physical retail supposedly up in the air, we wanted to find out how those who actually own retail real estate are feeling about the current climate. We sat down with investment sales teams from across the nation, who focus on all types of assets in different markets and in different regions of the country, to get their take on the current investment sales climate and to find out where things are heading in 2018.

The news is accurate, but many segments are still faring well

Investors would be foolish not to take the news of retail closures very seriously and to examine what could affect their bottom line. So it’s no surprise that vacancies at shopping centers, or the possibility for a store closure in the future, have made investors wary of certain asset types. These are namely power centers and regional malls, which are impacted as big box and anchor retailers continue to shutter stores.

“People are being very cautious of what they acquire right now,” said Pierce Mayson, principal of SRS’ Investment Properties Group. “They don’t want to get caught buying the wrong asset type and ending up in a bad situation. It’s not that there isn’t opportunity. Investors are just being cautious.”

“Everyone is seeing the big box closures this year and focused on how hard it would be to replace a tenant and fill that size space,” said Kyle Stonis, managing principal of the Investment Properties Group. “That has resulted in a thin buyer pool for that type of product, predominantly power centers in suburban middle markets.”

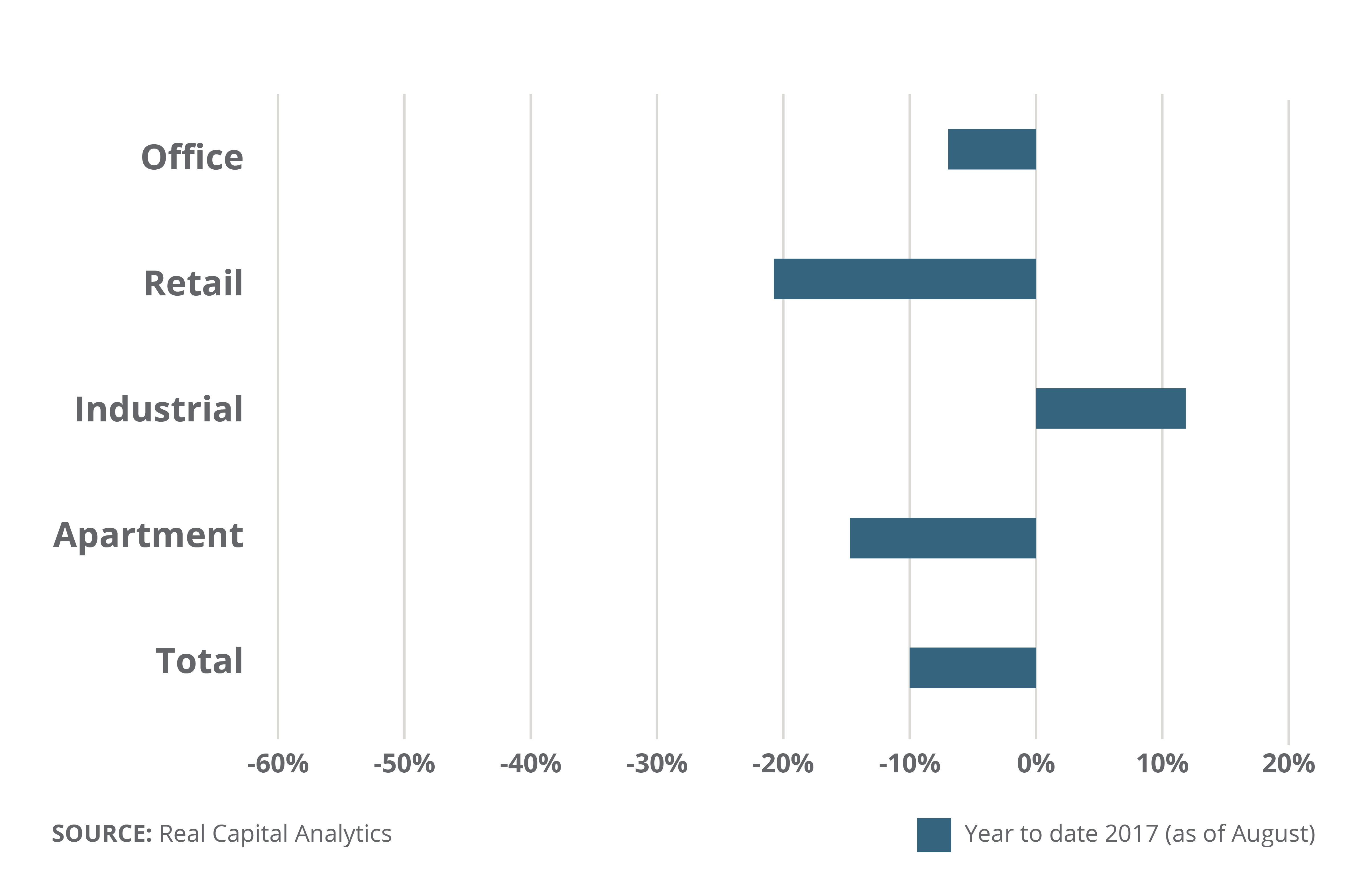

Year-Over-Year Change in U.S. Deal Volume

Our experts agree with industry assessments that investment volume has decreased by significant percentages, with Real Capital Analytics reporting a drop near 20%. As cap rates rise, sellers’ expectations are not being met, resulting in them hanging on to assets longer. But that is primarily playing out in suburban, secondary and tertiary markets, and varies from property to property.

“One thing to realize is that the activity and interest surrounding an asset is all very property-specific. One can be highly competitive where another could get no traction at all. It really depends on a lot of different factors,” said Mayson.

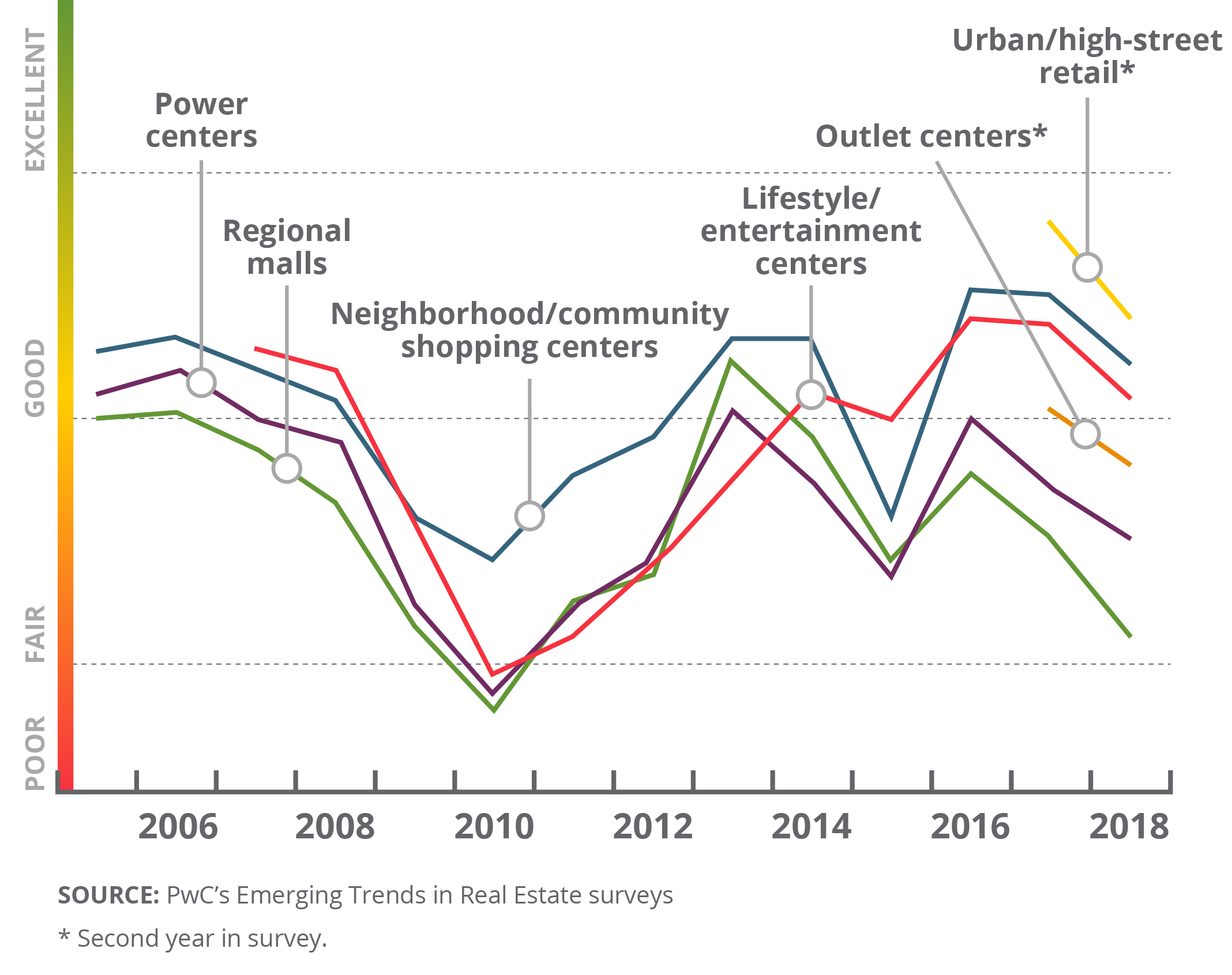

Additional information from PwC’s survey indicates that investment prospects for power centers are seen as fair to poor, while prospects for community centers, lifestyle centers, and urban centers are still considered good. This is a reflection of the trend toward experiential retail and attractions which go beyond the traditional shopping experience, which is more easily achieved in a lifestyle or urban center. Community centers are still holding strong as they aren’t typically dominated by multiple big-box retailers and have more of a focus on small shop space.

Retail Investment Prospect Trends

When interpreting the sales volume it is important to note that 2017’s drop is being compared to historically high numbers for investment property sales in 2015 and 2016 as both buyers and sellers benefitted from low interest rates. Even so, our investment sales teams feel that investors’ response to bigger tenant closures may be more of a knee-jerk reaction and feel confident heading into 2018 as things level off.

“What is actually having the most impact is debt and the low interest rates,” said Mayson. “We will see more capital deployed next year, and we’re watching what is happening with interest rates, but really it’s just a matter of people moving on from the initial shock of the retail closures and getting comfortable with the new norm.”

The news is also creating opportunity for retail investors

In spite of struggles in the retail industry, real estate investors are by no means turning away from retail opportunities. Retail will always hold a strong appeal for investors as earning potential is higher than other types of assets, and management requirements are lower.

“Despite the hits that retail has taken this year, there is still a lot of capital out there and interest rates are very low,” said Chris Tramontano, senior vice president in SRS’ Newport Beach office.

Recent news of Brookfield’s offer to purchase the remaining shares of General Growth Properties (GGP), whose portfolio mostly consists of “Class A” malls, is evidence that interest in retail assets is still quite strong.

“Brookfield’s offer shows there are groups out there that see an opportunity in the marketplace and want to acquire properties at good pricing with high cap rates,” said Mayson.

“In a sense there is a lot of energy generated by the whole ‘retail apocalypse’ idea,” said John Redfield, vice president in the Newport Beach office. “We are having more people looking to invest in retail because historically any time the media has talked badly about a sector, that sector seems to the have the most opportunity. The contrarian point of view plays a role in our industry. There is negative news out there, but quality assets are still very much sought after.”

Flight to quality means investors seek out core plus properties

As annual retail sales continue to grow, it is clear that physical stores are still profitable for retailers. As retail centers adjust and adapt to changing consumer preferences, investors remain attracted to well-conceived and well-positioned assets. The retail segments that are experiencing a boom are mostly focused in health and fitness, personal services, medical, beauty and grooming, and dining – all segments that cannot be easily replicated online. Properties that have a sufficient amount of these retailers are attractive to investors.

“Service oriented properties are sought after, and grocery anchored are the most desirable asset class for us right now,” said Tramontano.

These assets are generally considered to be investment, or institutional grade, suitable for large institutional buyers such as insurance companies, private equity firms or real estate investment trusts, or REITs. These assets tend to have more income-generating opportunities than smaller properties and chances to acquire those assets are plentiful for those who can raise the funds.

“A number of institutions are raising value add funds, but steering that money towards core plus assets as pricing has widened on those assets,” said Steve Miskew, managing principal of the Investment Properties Group and market leader in the South Florida office. “They are now able to buy those centers in the 7+ cap rate range and achieve yields they determine to be acceptable.”

Shannon Rex, senior director of the Debt & Equity Group also commented that “Institutions are paring back their underperforming assets and disposing of those in tertiary markets in preparation for peak of the cycle.” Interviewees from PwC’s Emerging Trends in Real Estate describe institutions as “fully invested,” and that institutional managers are feeling pressure as they sense values are nearing peak.

With any grade multi-tenant asset, investors are proving to be more comfortable with a constrained amount of space devoted to anchor versus small shop, in order to be prepared for more large tenant closures in the future.

“There used to be a preferred 70/30 anchor-space-to-small-shops ratio, but now investors are looking for the reverse,” said Redfield. Assets already with a healthy distribution of small shop space are extremely desirable.

“While traditional mall and power center cap rates have risen in the past year, multi-tenant small shops, particularly pads and outlots with smaller individual suites, tend to be in continual high demand now and into the foreseeable future,” said Patrick Luther, managing principal of SRS’ National Net Lease Group and Investment Properties Group.

Net lease properties thriving and considered an “internet shelter”

Not surprisingly, investors are looking to perceived ‘safer’ areas within retail to invest and net lease properties are a good place to find those retailers. In other words, investors are wanting to move into assets that are essentially “Amazon proof.”

“Quick serve restaurants, coffee shops, fast food, car maintenance, those essentially won’t be affected by Amazon,” said Greg Cline, vice president with the National Net Lease Group and a buyer representation and 1031 specialist. But opportunities extend beyond dining and services as well.

“Dollar stores are somewhat immune because of price point and accessibility,” said Cline. As for convenience to consumers, sometimes it is a matter of feasibility for delivery of online orders. Cline continued, “As you get into some areas it becomes more difficult for Amazon to make a delivery in 10 minutes.”

The demand for single tenant net lease properties is high right now, which is good for both buyers and sellers.

“Single tenant and pad sellers are still generally achieving their desired pricing,” said Matthew Mousavi, managing principal of SRS’ National Net Lease Group and Investment Properties Group. “Service and food oriented users are paying higher rents than ever before and are competing very aggressively for space.”

Doing the homework

One thing that is universal across all asset types and markets is that more research is required up front now more than ever before for financing.

“The underwriting and capital side is more challenging now. There is a lot more analysis, they are looking at sales, lease roll over, the position in relation to the competition, health ratios, and historical performance versus a forecast,” said Rex.

That sentiment is shared across all types of investors. “We’ve seen underwriting become more critical even from less sophisticated investor profiles. Buyers are asking for sales, not only of the stores within the asset, but of the greater region for the brand. If those sales numbers are not available, they often want to interview competing retailers or store managers,” said Luther. “There are just more boxes to check before a buyer will be comfortable proceeding today.”

Our experts also warn not to overlook larger retailers, even if it is perceived that they are struggling. “Sometimes it is misunderstood why a retailer is struggling. It could very much be an issue of overexpansion or corporate debt rather than issues with the concept itself. You need to look at where the debt has been placed, as the concept may still be solid, but they are being overlooked because of what is happening at the corporate level,” said Tramontano.

Rising rates in 2018

Watching and waiting seems to be the name of the game for some investors on both sides of the transaction. According to National Real Estate Investor’s latest finance survey, borrowers are optimistic despite some uncertainty about where financial regulation is heading and the impending increasing of interest rates.

Though evidence that a rise in interest rates has been imminent, sellers will start to feel a little more pressure to sell their assets. “It doesn’t make sense for sellers to sell when they can take advantage of debt and hold on to assets until the pricing is where they want it,” said Mayson.

Matthew Mousavi agrees that rising cap rates also cause sellers to cling to their properties, as interest rates have made the debt appealing. “On larger institutional or power center product, loan proceeds or the refinance options are often very competitive, compelling them to hold onto the property if they don’t achieve sale price execution.”

As to what that means as interest rates rise, Mayson comments that, “What we are seeing is that interest rates are going to rise a bit, and the debt will become less attractive. That will help owners decide they need to sell the asset.”

The majority of survey respondents felt that a rise in interest rates would cause cap rates to rise as well, which continues to benefit buyers. Rex agrees that, “Investors perceive cap rates increasing more briskly in non-core markets, the indicators are there.”

“Several of our buy-side clients are delaying any movement until the first quarter of next year to see if cap rates go up,” said Cline.

Respondents also expect capital sources across the board to have the same, if not more, debt capital available in 2018. PwC’s survey reported similar sentiment, predicting a “deep and diverse” pool of debt and equity capital expected to remain healthy for the foreseeable future.

“There are a couple of large institutions raising distressed debt funds as they anticipate the peak of the cycle due to rising interest rates and growing credit concerns,” said Rex. “Many retailers are struggling as the business cycle changes. However, a lot of the headlines are sensationalized and none of this appears cataclysmic.”

“Dollars allocated to retail investment by private as well as institutional investors will continue to need a home,” remarked Luther.

Tenant insight is key to preparation

As retail continues to evolve, perhaps the best course of action is to prepare for what to do if and when a tenant has to leave retail space. That’s where working with a team of investment property professionals gains you a significant advantage.

“We are constantly looking for ways to defend the rent roll and NOI replaceability with tenant rollover,” said Luther. “Much of this comes from our expertise within the tenant rep and leasing side of the business. We are able to show investors what types of alternative users are in the market for short term leases in centers they are acquiring. We also look at the options to recapture some of the space if a retailer wants to downsize.”

To leverage SRS’ retail investment expertise and tenant insight, contact Janie French who will connect you with the best Investment Services professional for your needs. Visit our investment services page to learn more.